The State is currently swimming in cash. At the end of 2024 the exchequer, buoyed by the receipt of the bulk of a massive tax payment from Apple, had a cash hoard of €34 billion, a full €10 billion higher than at the end of 2024.

This will climb further as the bulk of the additional €3 billion due from Apple arrives later this month. What to do with this is a vital issue in the coalition talks that are now under way.

It brings both opportunity and threat. The opportunity is obvious: to use the cash to underpin investment in housing, water, energy and other vital infrastructure, as well as to provide financial leeway for Ireland in the years ahead.

The threat is that the next government bases its spending plans on a gamble that corporation tax will keep flowing in – and then finds that it doesn’t.

READ MORE

As a once-off receipt of cash due to a European Court of Justice ruling, the Apple money should not be used to further boost State day-to-day spending. The exchequer finances are already over-reliant on this bounty. Using it to support further current spending means doubling down on the bet that the corporate tax gift will keep on giving.

Instead, the election manifestos of the main parties proposed that it be used to fund higher State investment spending in areas like housing in particular; investment spending, by its nature, is not a recurring bill and is thus a better home for once-off revenues.

In other words, using the Apple money to help build a new hospital makes sense, assuming there is a good case for doing so in the first place. Using it to help pay for the wages of the doctors, nurses and other staff does not.

Using the Apple money to help build a new hospital makes sense – assuming there is a good case for doing so in the first place. Using it to help pay for the wages of the doctors, nurses and other staff does not

In many ways, the dilemma caused by the Apple money landing in the exchequer and the huge cash hoard goes to the heart of the issues surrounding the management of the public finances.

On the face of it, Ireland’s budget figures are exceptionally strong, with Goodbody economist Dermot O’Leary estimating that the end-year surplus of revenue over spending is equivalent to over 7 per cent of national output (adjusted Gross National Income). Meanwhile, across much of the rest of the European Union, public finances are under pressure and budgets are in deficit.

But subtract from the figures the amount of corporation tax which the Department of Finance judges to be “windfall” – in other words related to multinational tax planning rather than real economic activity in Ireland – and the picture looks a bit different. O’Leary estimates that this turns a surplus of almost €13 billion last year into an underlying deficit of billion of €6.5 billion.

This goes to the heart of the dilemma: what can realistically be assumed for the next few years and how to deal with the spread of likely outcomes?

The political reality is that the cash just keeps coming in, even if the return of Donald Trump to the White House brings some clear and imminent dangers. The windfall element of corporate tax will not disappear overnight – indeed, the bulk of the money could continue to recur.

The point is that multinational restructuring, perhaps spurred by new US policies, could lead to corporate tax payments declining over a short period of years. And then the theoretical underlying deficit warned of by the Department of Finance might become something much more real.

It is worth digging a little into this week’s exchequer figures to see what they tell us about the underlying state of Ireland’s economy and the trends behind the key debates about budget policy

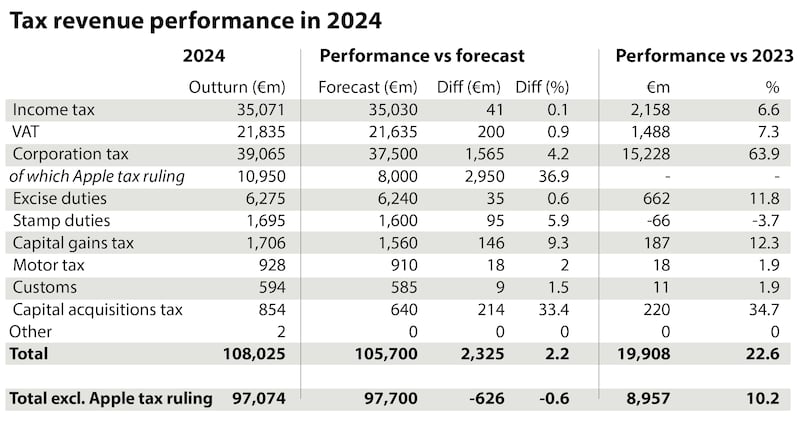

Income tax: This is a key indicator of overall economic health. It is up 7 per cent in 2024, reflecting a strong jobs market and rising incomes. Growth in recent years has been driven by the higher paid multinational sector and areas like professional services reliant on them. Strong PRSI receipts, meanwhile, are boosting the social insurance fund, which is in heavy surplus.

VAT: A vital pointer to consumer spending, also grew 7 per cent year on year. This is a key driver of overall economic activity.

Corporation tax: Receipts soared here by €15.2 billion to reach €39 billion. Subtract the €11 billion once-off Apple money and the total is around €28 billion, still up a healthy18 per cent on 2023, even if the rate of growth did fall below 10 per cent in the final quarter.

Spending: Total spending voted through the exchequer rose by a hefty 9.5 per cent to €103.7 billion. The Irish Fiscal Advisory Council, in a series of posts on X/Twitter, pointed to a series of overruns both in health and across a range of other departments. It has been critical of budgeting in health in particular – subject to annual significant overruns – and it warns that the budget allocation for health in 2025 again looks unrealistically low.

The bottom line: The exchequer surplus, which more or less measures the cash position of the State finances, was just under €13 billion in 2024. It is worth noting that if we ignore the Apple money, the surplus would fall to €1.8 billion.

The key EU borrowing measure, the general government balance, is calculated somewhat differently and will be estimated later. It will show the overall government finances remaining in significant surplus ,and this is forecast to continue into 2025.

The economy: It is difficult to draw back from all the complications underlying the figures. However, they indicate that the economy continues to grow strongly, with Davy Stockbrokers economist Kevin Timoney estimating that growth may have been around 4.5 per cent last year and could even have been a bit higher. Like the budget surpluses, this is in contrast to the performance across much of the euro zone.

So what happens next? The likelihood is that the State will continue to have a large cash pile over the next few years. Some is needed to provide leeway to the State and the National Treasury Management Agency (NTMA) in case unexpected trouble lands.

Some of the cash pile will be run down gradually to fund State investment spending, which – as outlined in the election manifestos – is set to increase further.

There was a big jump in State housing spending last year and more is likely from 2025 onwards, as well as additional spending in areas like energy and water, identified by the multinational sector as key weaknesses in Ireland’s current position.

In turn, used effectively, additional investment in housing and other infrastructure is vital to underpin further investment in Ireland, both from multinational firms and domestic players. And to improve the standard of living of the Irish people.

What’s in store for 2025?

This is the virtuous circle which the next programme for government should aim for.

There are other options. Some of the money could be used to pay down part of the national debt. This is unlikely: in other words, the State is unlikely to enter negotiations with lenders to pay back money early.

As much of it is longer-term borrowing at very low interest rates (the average interest rate on the debt is now just 1.4 per cent), this would probably not be worthwhile. However, if the budget remains in surplus, the NTMA will only have to borrow to roll over maturing debt.

And some of this could conceivably be funded from the cash pile too, rather than taking on new loans. This is another way of effectively chipping away at Ireland’s debt pile, which is close to €220 billion.

The next government could also decide to put some of the extra cash from the Apple receipts into two new funds established by the outgoing administration to help pay future bills.

The economy is at full capacity, and shortages of construction workers, engineers, building companies, planners and so on make additional investment spending challenging to pull off

With around €7 billion due to go into these funds next year anyway, this may be seen as sufficient. But there is an argument, too, for bumping up the funds through a one-off payment from the Apple receipts to underpin the exchequer in later years.

The main political decision, however, is likely to be to use a lot of the cash to fund vital investment over the next few years. There are, of course, significant challenges to doing this.

The economy is at full capacity, and shortages of construction workers, engineers, building companies, planners and so on makes additional investment spending challenging to pull off. The risk is of overheating the economy or getting poor value for the State. Or both.

These delivery challenges are central for the next government. The complications of establishing a new department of infrastructure to oversee this, as proposed by Fine Gael, or giving responsibility to the NTMA to oversee delivery, as Fianna Fáil called for, will now be surfacing in the coalition talks. Ireland, right now, has the cash – it is delivery which is the real challenge.

And then there is the risk from a shock to tax receipts starting to tighten the budgetary position during the next government’s term.

Ensuring money goes in to the two State funds, keeping the budget in surplus and maintaining a large cash pile would all help to give the State leeway to maintain investment spending if this happened, without having to resort to painful cuts elsewhere.

To achieve all this, the new programme needs to involve a financial framework for government which the next administration will actually stick to. The last one largely ignored the spending “rules” which it set itself.

This would control the growth of current spending and ensure that budget surpluses were maintained and that payments into the two funds for the future continued.

If economic growth remained strong, revenues would continue to improve Ireland’s cash position – for example, boosting the social insurance fund further. And there would be scope to adjust if things took a turn for the worse.

If there is one lesson from the financial crash, it is how quickly Ireland’s national finances can get into trouble if things do go wrong

It is up to Ireland to decide what to do here and how a new budget framework would operate, as it does not appear that the new EU budget rules will have much impact on Ireland’s decisions over the next few years, even though they are intended to promote sensible budgeting.

The strong position now gives what may be a singular opportunity both to boost investment and to underpin the national finances for the years to come, thus taking out some insurance against another boom-and-bust cycle occurring. If there is one lesson from the financial crash, it is how quickly Ireland’s national finances can get into trouble if things do go wrong.

Blowing this chance by frittering money on giveaways and having no real control on the annual budget, or on a proper longer-term strategy, would be a big mistake. It would waste what may well be a once-in-a-generation opportunity to do the right thing.

- Sign up for the Business Today newsletter and get the latest business news and commentary in your inbox every weekday morning

- Opt in to Business push alerts and have the best news, analysis and comment delivered directly to your phone

- Join The Irish Times on WhatsApp and stay up to date

- Our Inside Business podcast is published weekly – Find the latest episode here