Policy on savings is not usually noted as a general election winner. But a number of parties are believed to be looking at the issue for their manifestos. With more than €150 billion of household savings sitting in bank accounts, according to the latest Central Bank figures, there are policy reasons for trying to attract some of it into equity-type investments – both to provide a better return for investors, and to channel money into Irish businesses.

Election manifestos can take two broad approaches. One is to remove the existing barriers to investing in a variety of funds, largely related to how they are taxed. The second – with echoes of the SSIA scheme that provided State incentives for people to save in 2001/2002 – is to provide some kind of tax break for people to move their money from savings to equity type investments. In its pre-election document this week, Chambers Ireland, the umbrella body for chambers of commerce, suggests developing “tax-incentivised investment channels that encourage these deposits to support more indigenous business growth, infrastructure expansion and green energy projects.”

Above all, simplicity is vital in whatever is brought forward, in an area which has become overly complex for retail investors.

1. The issue

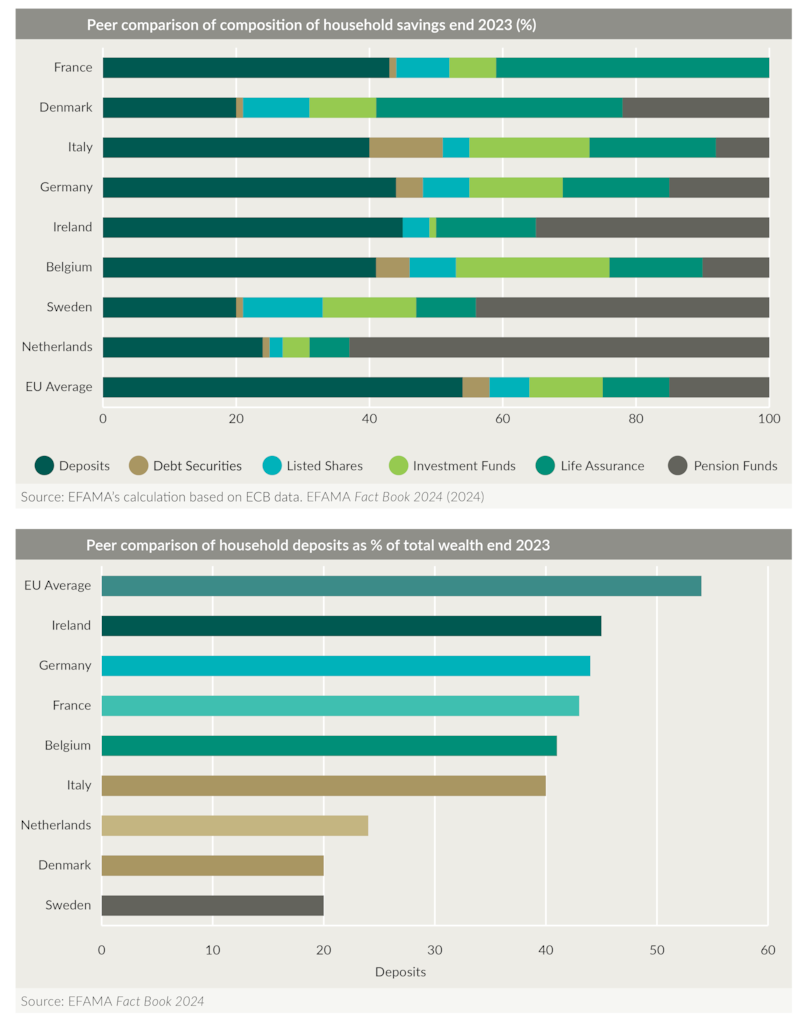

Irish people tend to put their savings in the bank and most participate in equity markets only indirectly, via their pension or life assurance funds. As the retail section of the major Department of Finance study on funds published recently pointed out, “in general the proportion of Irish households’ financial assets held directly in investment funds, listed shares and securities is much lower than in many other countries”.

READ MORE

The report argued that there is a need for people to build savings and investments, including pensions, for “life events”, and also for some of these savings to be used to support real economic activity. The EU, via its capital markets strategy, also wants to encourage more retail investment in capital markets, and member states are being encouraged to examine policies to encourage this.

Over the longer-term, investments in markets have generally done better than those in deposit accounts, despite short-term ups and downs. So a policy issue is to encourage people to shift money from generally lower-yielding savings accounts into equities, to help them provide for their financial future. And doing this via funds generally involves lower risk than putting cash into individual equities.

We should note that the Department of Finance’s review advised against moving into this area of incentivised schemes until the basic tax issues hindering investment had been dealt with

2. The quick “fixes”

Government policy plays a role in where people put their money. In particular, the taxation of investment funds such as Exchange Traded Funds (ETFs) – a quoted fund which typically tracks a particular stock market index – and life assurance-linked products is problematic. While there are complex issues in the tax treatment of funds, the department’s report focused on a few key issues.

One is that after eight years of investments being held in such a fund, Revenue rules are that tax must be paid on any gains as if the shares were being sold – a “deemed disposal” in the jargon. The report recommended that this be ended, and that tax be paid on gains when sales take place.

The second issue is that tax on income arising from distributions from such funds is high – 41 per cent in the case of ETFs, compared to a 33 per cent capital gains tax rate on profits from gains on individual shares. The Department of Finance report said the tax rate on profits from funds should be cut to 33 per cent, so that the same treatment applied. An issue for the thousands who have invested in ETFs is also that they are obliged to include this in a tax return and complex rules can apply here, particularly in relation to offshore products.

The report also called for a 1 per cent levy on life assurance products – long a bugbear of the industry since its introduction in 2009 – to be removed. And for investors to be able to write off losses on the holding of these funds for capital gains tax purposes, which is not allowed under current rules and again differs from the rules applying to individual shareholdings. Conscious of the cost, the Department of Finance officials who wrote the report called for these changes to be phased in over a period of years.

A key argument for changing the tax regime is that it would encourage people to invest in diversified funds – with lower risk – rather than in individual equities. Many ETFs, easily available online, also offer relatively low charges to investors, and this is important as investment managers often take hefty fees which cut the benefit to small investors.

3. The SSIA-style route

Would these tax changes be enough to get money out of savings accounts? There will also be consideration of whether to provide incentives via the tax system for people to move savings into equity investments.

Here the most obvious model is the UK Isa regime, though the funds review also referred to schemes in Sweden, Italy, Canada and elsewhere.

The UK scheme offers tax free returns on investments of up to £20,000 (€24,000) per year in savings, stocks, bonds and a range of other investments, and some kind of tax-free structure would seem the obvious way of providing an incentive here.

Above all, simplicity is vital in whatever is brought forward in an area which has become overly complex for retail investors

A new proposal for a special Isa offering an additional £5,000 (€6,000) each year for cash put specifically into UK companies was canned in this week’s British budget. There are separate schemes for those saving to buy a home or for retirement, including a bonus element, but specific rules apply here on withdrawing money. Interestingly, in the manifesto for the last election, Fianna Fáil proposed a special savings scheme for those looking to buy a home. The Isa scheme has been seen as overly-complex and the incentives for people to invest in cash, as well as equities, appear perverse and would not feature in any Irish scheme.

While EU rules would probably mean that any “tax-free” incentives here would need to apply to investments made across the union, there would be nothing stopping Irish banks or brokers promoting products which put cash into Irish companies, or – as mentioned in the department’s review – provided funding for key sustainability projects.

It would be a way of investors getting access to Irish businesses likely to work better than the old Business Expansion Scheme which offered a tax break for investing in one company. Some of these did not end well.

There are issues to be considered. Few Irish companies are quoted, and cash put into non-quoted companies or specific projects is riskier and not as liquid. Also, rules would be needed to protect investors and make sure they were aware of any risks. Fees could also be high, cutting return.

We should note that the department’s review advised against moving into this area of incentivised schemes until the basic tax issues hindering investment had been dealt with. Normally, politicians would listen. But with a general election in prospect, some may well choose to propose something more innovative.