Rental growth has slowed, but rents are still rising and – averaging just over €1,400 per month – remain among the highest in Europe. And not only is the average level of rents high, but research confirms what anyone looking for an apartment knows – there are few cheaper properties available. There are signs of supply increasing but much more is needed if rents are to not to remain at levels that are unaffordable for many. And the crunch issue remains – we can’t seem to build apartments at an affordable cost. Here is the problem in five graphs.

1. Soaring rents and apartment living

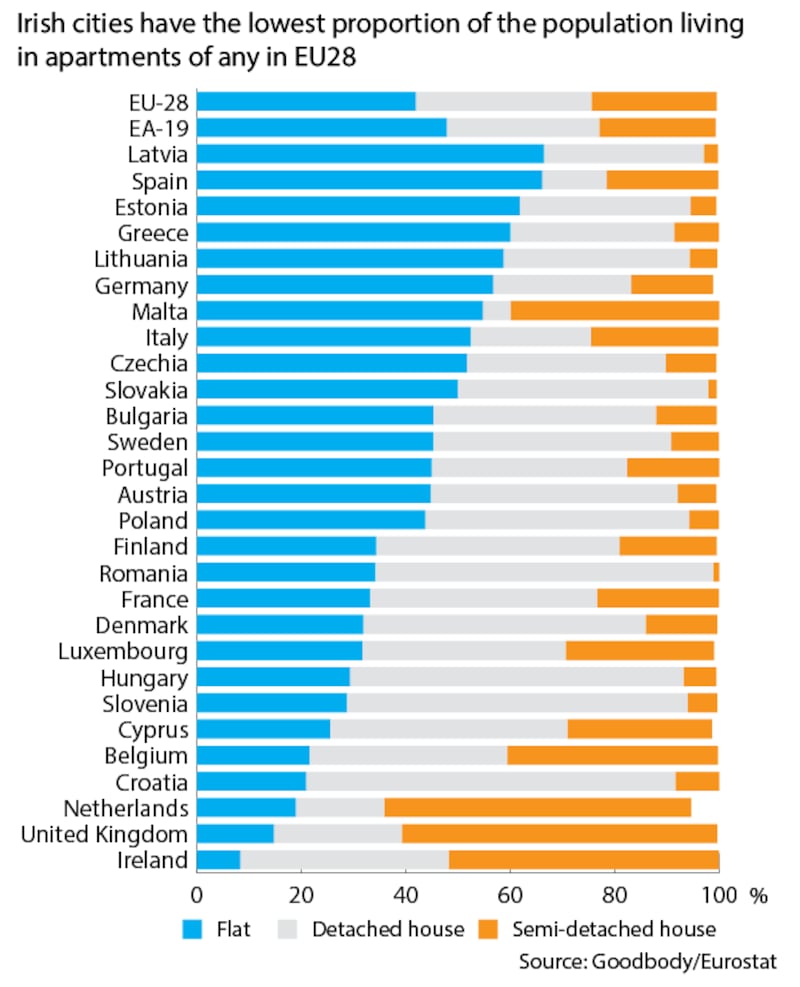

The rise in rents is slowing – finally – after an extraordinary rise. According to the latest report from Daft.ie, the annual increase in rents has fallen from 12 per cent in mid-2008 to 5.2 per cent now. In Dublin, the rental inflation rate has fallen to just below 4 per cent. But prices are already at a level which are unaffordable for many – and a stretch for others. As economist Ronan Lyons points out in the report, rents in Dublin have more than doubled since bottoming out in 2010. Slowing rental growth now appears to reflect an increase in supply onto the market of rental properties – this increase is welcome, though supply remains below potential demand. And while the latest housebuilding statistics have shown an increase in commencements, analysts believe that supply will remain well below demand for some time to come and that the key issue – how to deliver affordable apartments – still has to be cracked. This is a big issue as a key part of the Government's spatial plan is to have more people living in apartments closer to city centres. As the graph shows, apartment living, while it has risen over recent years, is still much less popular here than elsewhere in Europe.

2. Affordability crux

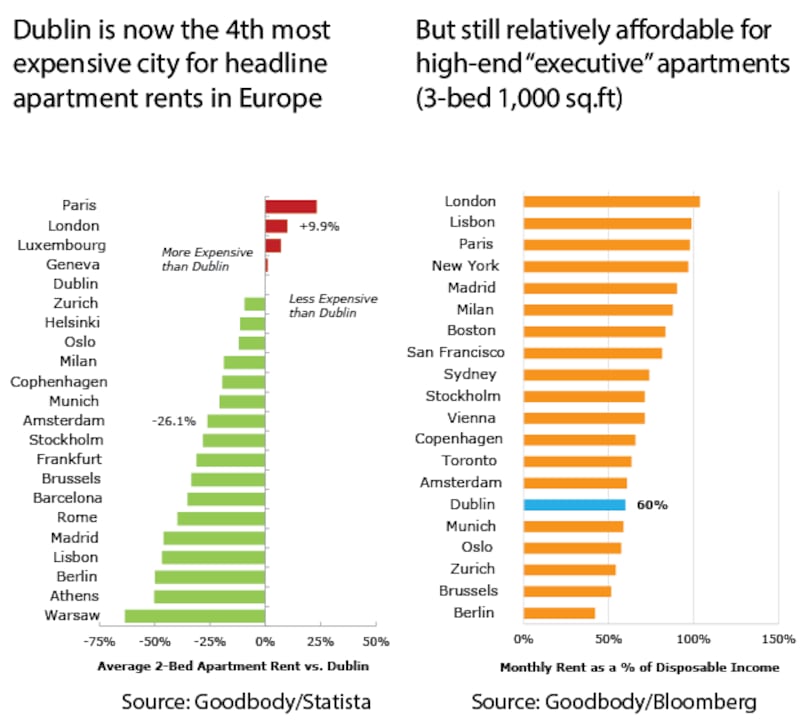

There is no difficulty demonstrating that rents here are now high compared with incomes – or with other countries. Analysis by Goodbody puts typical Dublin city centre apartment rents at 55 per cent of average disposable income, well above the level of around one-third which is generally seen to be sustainable. So for those on average incomes, city centre properties are unaffordable to rent.

In Europe, comparisons vary depending on exactly what data is used, but generally show only Paris, London, Luxembourg and Geneva similar or more expensive than Dublin. According to a recent AIB presentation, using Eurostat data, headline rents here are way ahead of major centres such as Brussels, Rome and Madrid.

Up to recently, rental growth was moving way ahead of the rise in incomes – and so affordability was worsening. ESRI research has shown a widespread rent-affordability problem at lower incomes, with lower-earners typically having paid over 40 per cent of disposable income in rent – and this figure will have risen for many in the last couple of years. They argue there is a structural, long-term problem here, being made worse by the economic cycle.

Interestingly, at the other end of the spectrum, the Goodbody analysis finds that for the high-end apartments – three-bed luxury apartments in the Docklands, for example – Dublin is not particularly expensive compared with other major cities. People at the higher income levels looking at such properties can afford to spend a higher percentage of disposable income on accommodation and still have plenty left to live on.

3. Historical perspective

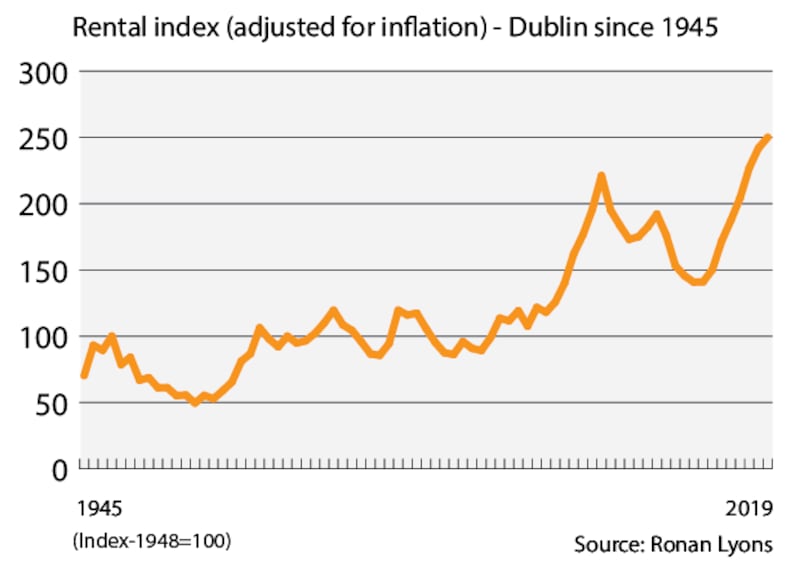

The debate about housing costs frequently involves older generations pointing out that housing was also expensive when they were starting out. However, research by TCD economist Lyons suggested that, looking at rental levels going back to the 1940s, the inflation-adjusted cost is now clearly at a peak. Only now, as rental growth slows, will income growth – for some at least – move ahead, thus slowly improving affordability. For this process to accelerate, rents would have to actually fall, which could of course happen, but typically has only done so during a wider economic crisis which also puts pressure on incomes. A consistent increase in supply, at the right price levels, would be the only way to break the cycle. And the risk – in the current market structure – is that falling rents would in themselves hit supply by lowering returns for landlords, either private landlords or the big institutional investors now becoming more important in the market.

4. Market crunch

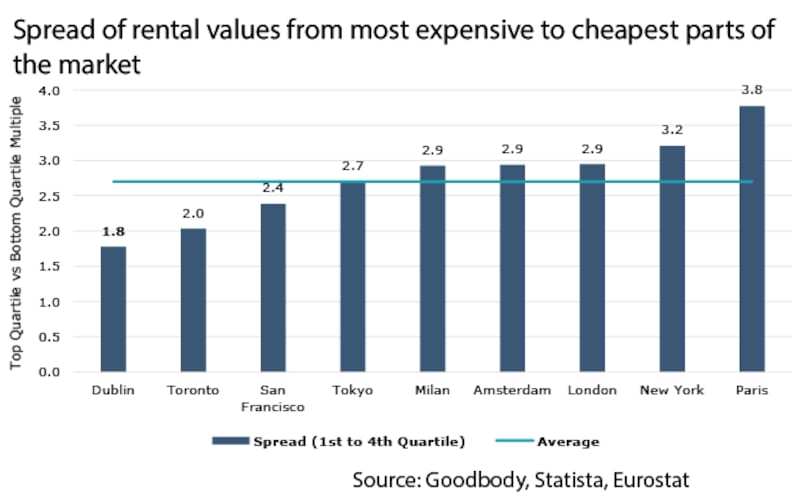

A healthy rental market offers a range of options – in terms of quality, location and price. Speaking at a recent Urban Land Institute conference in Dublin, Pat O’Sullivan of AIB referred to Goodbody research showing a relatively narrow gap between the most expensive and the cheapest rentals in Dublin. Here rents at the top end are about 1.8 times those at the lower end, compared with 2.5-3.5 times in most other major markets.

What this means is that not only are average prices high here, but also that lower-priced apartments here are proportionally more expensive than in other markets. In other words, such is the shortage that even lower-quality apartments are dear and there is little by way of cheaper, or starter, rental supply.

This has led many to have to rent a bed with others in an apartment or house, rather than having an apartment of their own – the so-called “crammers.”

5. The price crux

Normally high prices in a market place lead to increased supply and so price growth moderates. There are some signs of increased supply in the Irish housing market. Government initiatives relating to the use of State land – centred around the new Land Development Agency – and the impact of changed building regulations should all help, in time at least.

But a problem a long time in the making will not be solved quickly – and there is a real crux in relation to the price of delivering apartments. Central to this is the price of building stand-alone apartment developments, with the cost of development inevitably pushing the apartments into higher price brackets.

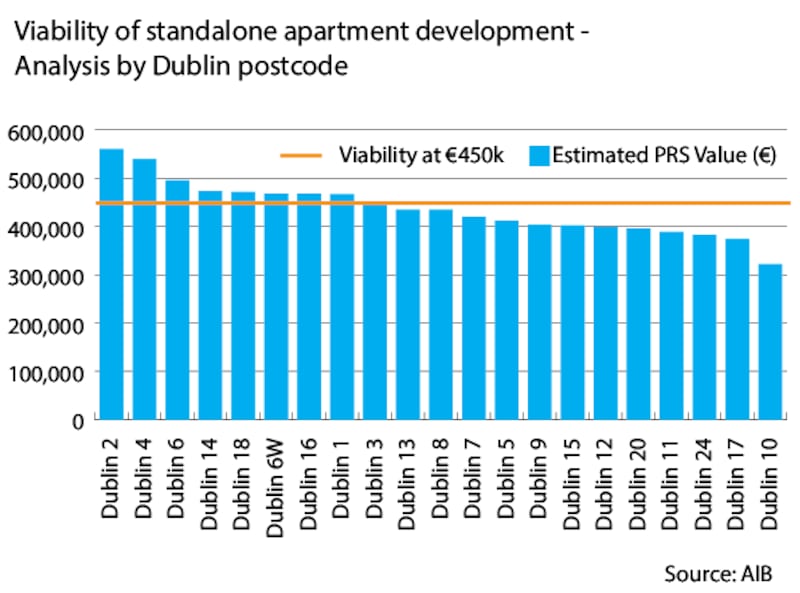

AIB's analysis, based on an apartment selling price of €450,000 which is seen as a rough guide to what is needed to deliver a return to the developer, shows that outside Dublin 2, 4 and 6, viability is challenging at best, and absent in many cases. Income levels simply do not support the apartment price necessary to get a return, given the income limits imposed on borrowers by Central Bank rules. Meanwhile, in Cork, incredibly, no apartment block has been completed in the past decade, though a number are now in development.

The central question is why apartment building costs here are so high. Economist Lyons writes that Government here cannot rely on international investors as the only answer to providing apartments. These investors have been attracted here by high-rent levels and builders have locked in returns by selling developments to them to rent on. The industry argues that this has underpinned an increase in supply – which it has – but the resulting rentals are generally aimed at the better off. Despite rising rents, meanwhile, private landlords are pulling out, blaming increasing regulation, controls on rents and taxes.

So in terms of affordable rental properties, we still need a model which can deliver – and which changes the maths which all too often now favour commercial development or even student accommodation. Policymakers “need to figure out why it is so expensive to build in this country and tackle that head on”, says Lyons.

The industry points at regulation, taxes, planning and the costs of doing business here. Government sources say the industry needs to up its game in terms of design and delivery – and that Government initiatives will gradually bear fruit as “brownfield” former industrial sites closer to the city centre come on stream together with new public/private initiatives.

Central to the Government’s approach is to have more people living closer to city centres, with a shorter commute and access to facilities and public transport encouraging people to live in smaller homes, whether apartments or small houses. If this is to work, a way simply has to be found to build the required multi-unit developments at prices which people on average incomes can afford, possibly helped by some new models with State involvement.