How on earth are investors meant to manage in the world where stock markets – at least in the short term – are driven not by the fundamentals of earnings and the economic outlook but by the latest outpouring on Truth Social from Donald Trump?

Markets rose this week after Trump moved to allay fears that he would seek the dismissal of Federal Reserve Board chair Jay Powell and also said that he expected tariffs on China would “come down substantially” from their current stratospheric levels. It is the latest shift – apparently in response to market fears that had led to renewed pressure on equities and bonds and the safe haven of gold soaring to record levels.

[ Explainer: what’s Trump’s beef with US Fed chairman Jerome Powell?Opens in new window ]

But there is little consensus on where markets go from here. So what should investors watch? And is there a wider story behind the relentless Trump news flow?

1. Glass half-full or half-empty?

As the rollercoaster ride of markets – particularly in the US – has shown, there is no settled view on the likely trend. This week, senior analysts at Goldman Sachs warned that in their view the risk of a US recession was still “underpriced” and this “leaves markets vulnerable to any signs that a recession is materialising”. Striking a more optimistic view, UBS said that, while downside risks remain, recent demonstrations that Trump is prepared to be flexible on tariffs and the likelihood of deals being struck in the 90-day period of talks set by the US administration to make progress “should encourage investors to look through near-term tariff-induced economic weakness and toward a return to earnings growth in 2026″.

READ MORE

So is the glass half-full or half-empty? Certainly investors remain nervous and uncertain and the underlying issue of a possible withdrawal from US assets by international investors continues to rattle around the markets. Some analysts believe this narrative is overdone – but how the tensions between Trump and Powell play out may tell a lot.

2. Normalising the new world?

The swings in Trump’s policies suggest that the president wants to use his first two years – before the midterm elections – to remake the US and the world trading system, but lacks a detailed strategy to make either of these things happen. This does not necessarily mean he will fail, but it suggests that the uncertainty of major changes being tried and then partly pulled back on may continue.

What investors need to watch here is that, despite the reversals, fundamental changes may stick. It remains unclear, for example, whether Trump is prepared to negotiate away all the tariffs he has imposed or threatened. Does he, as some statements from the administration have indicated, see the 10 per cent tariff now in place on trade from many countries as a baseline that will stay in place for the long-term, to encourage production back to the US and raise money for the US exchequer? And while tariffs with China may fall, when might this happen and what might the terms be?

The point is that while the remaining 10 per cent tariffs are being largely ignored in the debate about whether higher tariffs can be avoided, in themselves they are significant, will push up US inflation and have led analysts to slash US growth forecasts. Goldman Sachs now see US GDP growth at just 0.5 per cent this year, with a 45 per cent chance of a recession. Normally this would be bad for equities and good for fixed income – such as bonds – though the recent “sell America” trend has seen US government bonds sell off, too.

[ IMF warns tariffs will result in big shock to global growthOpens in new window ]

While Trump has withdrawn the threat to try to dismiss Powell, the hectoring to tell him to reduce interest rates will continue. And this is part of a wider story as Trump’s attempts to remake the US continue apace, as shown most recently in his attack on universities, tougher immigration policy – including for visitors – and crackdowns on those with opposing views on the administration on issues such as Israel and attacks on the judiciary. Again, despite rowbacks, fundamental change may stick. To the extent that investors – both in US assets and industrial projects – favour predictability and rationality, this backdrop is important, as is the dismantling of key parts of the public service and the research base. How big global US multinationals cope with this in their investment strategies will be interesting to watch. They are being incentivised to produce “at home” for US markets, but they are global entities with international supply chains and will ultimately act purely in their interest of shareholders.

3. A low growth era?

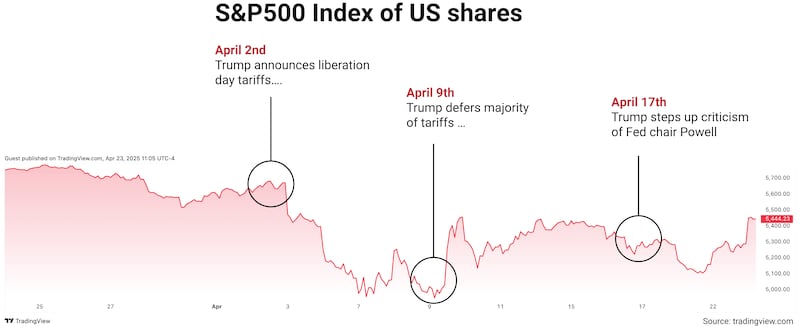

Trump’s policies are a “negative shock”, as the IMF has noted. And the risk of a wider trade war remains. While there is talk of a string of trade deals between the US and other countries, a more likely outcome is an ongoing process of deals in some cases and conflict in others, with tariffs – and threats of tariffs – coming and going. Another key thing to watch is that there seems to be discord in the Trump camp on the tariff strategy. How this plays out will be vital for markets – and the world economy in general. The US tariff strategy is promoted by senior adviser Peter Navarro while treasury secretary Scott Bessent is taking a more cautious approach in public and is believed to have persuaded Trump of the need to delay the implementation of much of the “Liberation Day” package of April 2nd. This row back occurred one week later on April 9th.

But US economists such as Nobel Prize winner Paul Krugman warn that it will be very difficult to end the crippling uncertainty now damaging confidence and thus putting investments on hold across the US and in many other countries. The genie is out of the bottle and the swings in Trump’s policies appear endless.

[ Tariffs and your pension pot: Whatever you do, don’t look nowOpens in new window ]

The wider point is that growth in both the US and EU now looks set to be below 1 per cent this year as things stand, meaning recession is a risk if trade tensions build. This would point to lower official interest rates on both side of the Atlantic, even if tariffs do push up inflation a bit. The IMF sees a 40 per cent chance of a global recession.

4. Has Trump already lost?

The US president is caught in a bind. He has shown weakness by partly-reversing his April 2nd tariff announcement and his implicit threat to get rid of Powell. If he tries to double down on tariff threats, he risks creating another run on the market, including not only equities but also the US treasury market, one of the bedrocks of the international financial system. Some analysts feel that the perceived threat to the so-called plumbing of the US financial system has been overblown. But it is impossible to know for sure – the risks lie deep in places such as the trading practices of highly leveraged hedge funds, or other parts of the system hidden from view. It was an obscure trade undertaken by pension funds that upended the Liz Truss government in the UK. And even though he has - for now at least-withdrawn the threat of trying to remove Jerome Powell, his endless pressure to cut interest rates can only chip away at the perceived independence of US monetary policy and investors’ confidence it in.

The price of US government debt is also vital to Trump as it determines the cost of refinancing US government debt – about $7 trillion of the total $36 trillion debt must be refinanced this year. And with a big budget deficit and a debt pile that is now at the limit agreed with Congress- and tax revenues set to slow along with the economy- the public finance situation is on a tightrope. A series of crunch points lies ahead, including the need to raise the debt limit, and that will require agreements with Congress. Slow growth will make this much more difficult and makes the treasury’s target of cutting the deficit from over 6 per cent now to 3 per cent by 2028 really challenging. Add in the need to find a way of refinancing the 2017 tax cuts package, which Trump has promised to do, and the risks to the public finance outlook rise further.

So there is a rising possibility that the US president is now in a bind largely of his own making from which he will find it hard to plot a way out. The most likely escape route would be to row back on the tariffs with a series of quick deals (which inevitably would not mean too much) and change course. But doing multiple deals in 90 days looks impossible.

For now, the US president may stick with his policies – but if the economy slides towards recession and the markets get nasty again, the pressure will only to grow.